BY JOSEPHINE CHINELE & ZUZA NAZARUK

Micheal Msukwa, a tobacco farmer and chairman of over 30 farming clubs in Malawi’s Northern region, is among those who claim to supply their crop to Alliance One Tobacco Malawi (AOTM), the country’s second-biggest tobacco leaf buyer. After years of contract farming for the company, Msukwa and his peers have seen little benefit.

Our five-month-long investigation suggests that AOTM may be providing ‘unlawful and dangerous’ working conditions to its farmers, alongside allegations of paying minimal to no income tax in Malawi. These findings raise serious questions about the company’s operations and adherence to local and international corporate standards.

“I wouldn’t be surprised to hear that these companies are not paying our government what they are supposed to pay,” Msukwa stated. “The duty-bearers are aware that these companies are not paying enough, but someone may be benefiting from these deals at the expense of our sweat.”

This situation not only highlights the struggles faced by local farmers like Msukwa but also points to larger issues of corporate responsibility and economic justice in developing economies. The impact of such tax practices on Malawi’s economy and its citizens is a matter of significant concern, calling for further scrutiny and action by both local and international bodies.

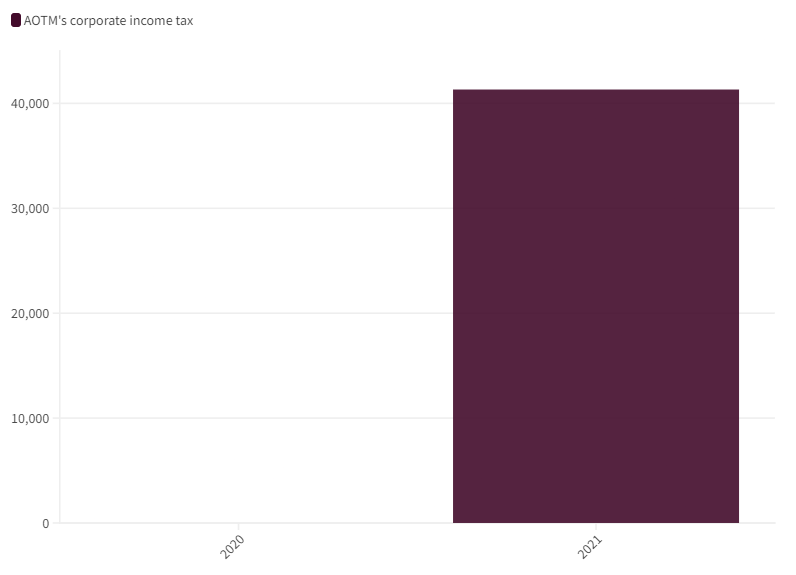

Zero Corporate Income Tax Paid by AOTM in 2020

A confidential document leaked from the Malawi Revenue Authority (MRA) has shed light on the tax payments of Alliance One Tobacco Malawi (AOTM) between January 2020 and September 2021. The document details various tax contributions by AOTM, including pay-as-you-earn, withholding tax, and notably, corporate income tax (CIT).

Strikingly, the records reveal that AOTM did not pay any corporate income tax: not even a single kwacha (the currency of Malawi): in the year 2020. This revelation raises significant questions about the company’s fiscal responsibilities and practices in Malawi, a country where tax contributions from multinational corporations are vital for national development and social welfare programs.

Alliance One Malawi Tobacco’s corporate income tax per leaked document from the MRA. Graphic by Zuza Nazaruk

Malawi-based companies should pay 30% of CIT on their profits. Profits remain after costs – of running operations or buying products for re-sale, for example – are deducted from the total revenue on goods sold.

Several experts suggest that not paying CIT could mean the company has not been turning a profit. This is highly unlikely, given AOTM’s importance in the global tobacco market.

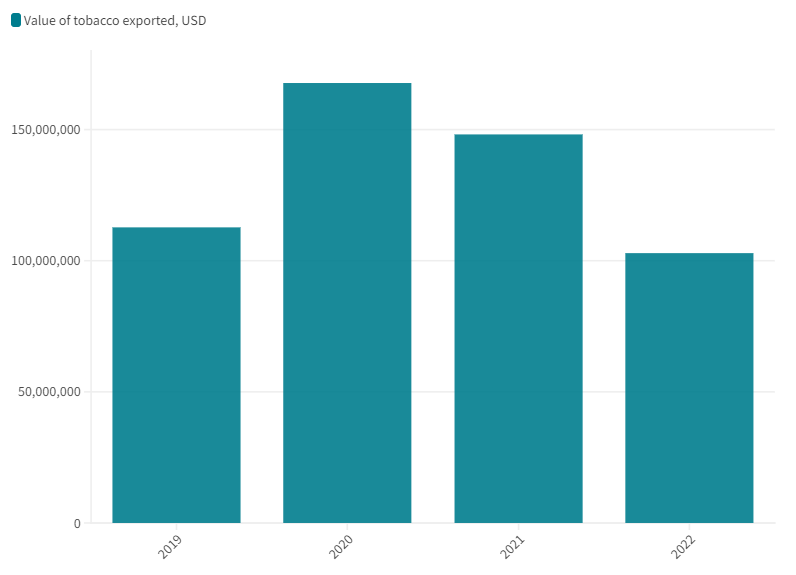

AOTM is Malawi’s second-largest tobacco leaf buyer, accounting for about 40 per cent of the market share. It’s also one of the key revenue providers for its parent company, a US multinational, Pyxus International. We analysed trade data, which shows that in 2020, AOTM exported over 168 million dollars’ worth of tobacco.

Total value of tobacco exports by Alliance One Tobacco Malawi between 2019-2022, per trade data. Analysis by Zuza Nazaruk

Pyxus and Universal Corporation are the only two publicly traded leaf merchants worldwide. Pyxus trades under the more recognisable name Alliance One. Leaf-buying companies purchase tobacco directly from farmers and sell it to cigarette manufacturers, such as Philip Morris or Imperial Tobacco. As intermediaries between raw and finished products, leaf buyers are the backbone of global tobacco production. Their role is so important that they “have pre-arranged contracts with cigarette manufacturers to provide them with a certain amount of leaf that the cigarette companies require meeting their demand for production,” explains Marty Otañez, an anthropology professor at the University of Colorado Denver, who spent years researching the tobacco sector in Malawi.

No Annual Reports

Where are AOTM’s profits going, then? Such information figures in annual reports, where companies declare various aspects of their finances. Both AOTM and MRA, however, declined to share the reports with us despite our sending multiple official requests.

As a subsidiary of a US multinational, AOTM is not obliged to publish their annual reports. Francoise Malila, AOTM’s Corporate Affairs Manager, stated, “Our [AOTM’s] contributions are consolidated and publicly reported quarterly on a global scale.”

All Malawi companies must file annual reports with the Registrar General, an entity responsible for the registration and administration of business entities. The export proceeds of AOTM are registered with the Reserve Bank of Malawi (RBM), Registrar General Office, and MRA.

We could not obtain AOTM’s financial records even after filing an official search request with the Registrar General’s office. MRA denied commenting on this issue. “Taxpayer matters are confidential, and we cannot give out such information,” said MRA Manager-Marketing Communications, Wilma Chalulu.

“Failing to provide [the company’s] financial reports to Malawian citizens is a red flag,” Wales Chigwenembe, a social accountability expert from Malawi, said. “Multinational companies usually use their global [presence] to dodge tax, among other financial crimes. They’re operating in Malawi, profiting from the country’s important crop. Why should they hide their reports through international parent companies?”

High Payments Abroad

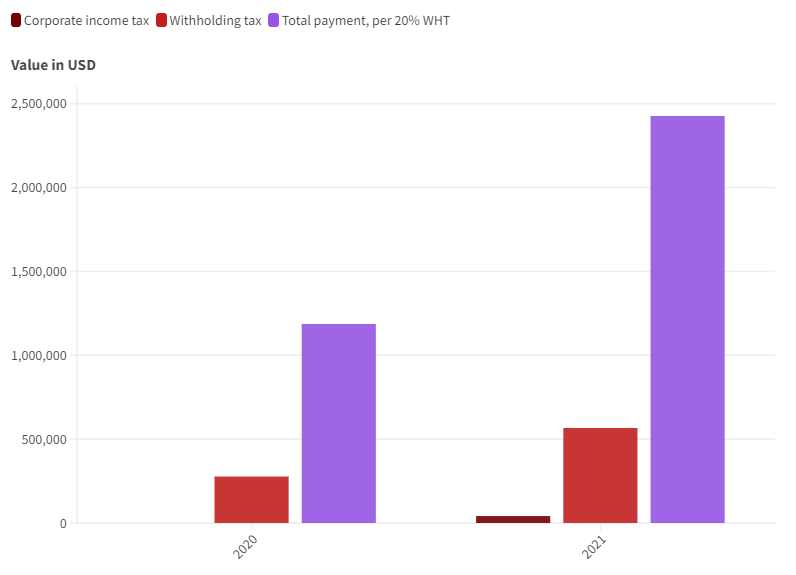

Without yearly reports, we turned to other tax payments in the leaked document. Experts we interviewed: Bob Michel, comparative policy and legal analyst at Tax Justice Network, and Vincent Kiezebrink, researcher at the Centre for Research on Multinational Corporations SOMO – pointed out the high volume of withholding tax (WHT) payments. “WHT are a levy on payments to foreign entities, specifically, dividend, royalty, or interest payments, and then management or technical fees,” Kiezebrink explained.

“Those payments are made with taxable profits,” Michel added. “So they reduce the tax base in the country.” For this reason, Kiezebrink stated, payments with levied WHT are “often used to shift profits and avoid taxes.”

In Malawi, the WHT rate is 20%. Data we analysed on payments made abroad shows that in 2020, the year AOTM paid zero corporate income tax, it made payments of over 1.1 million USD abroad. In 2021, when the company paid just over 41,000 USD in corporate income tax, it paid over 2.4 million USD abroad until October 2021. As the leaked document contains another column for dividends, these payments were either for interest on loan, management or technical fees.

“Th[ese payment volumes] mean that the company [AOTM] has profit, and a lot of this profit is turned into expenses that go abroad,” Michel stated.

Comparison of AOTM’s corporate income tax, withholding tax, and WHT-subject payments abroad. Analysis by Zuza Nazaruk

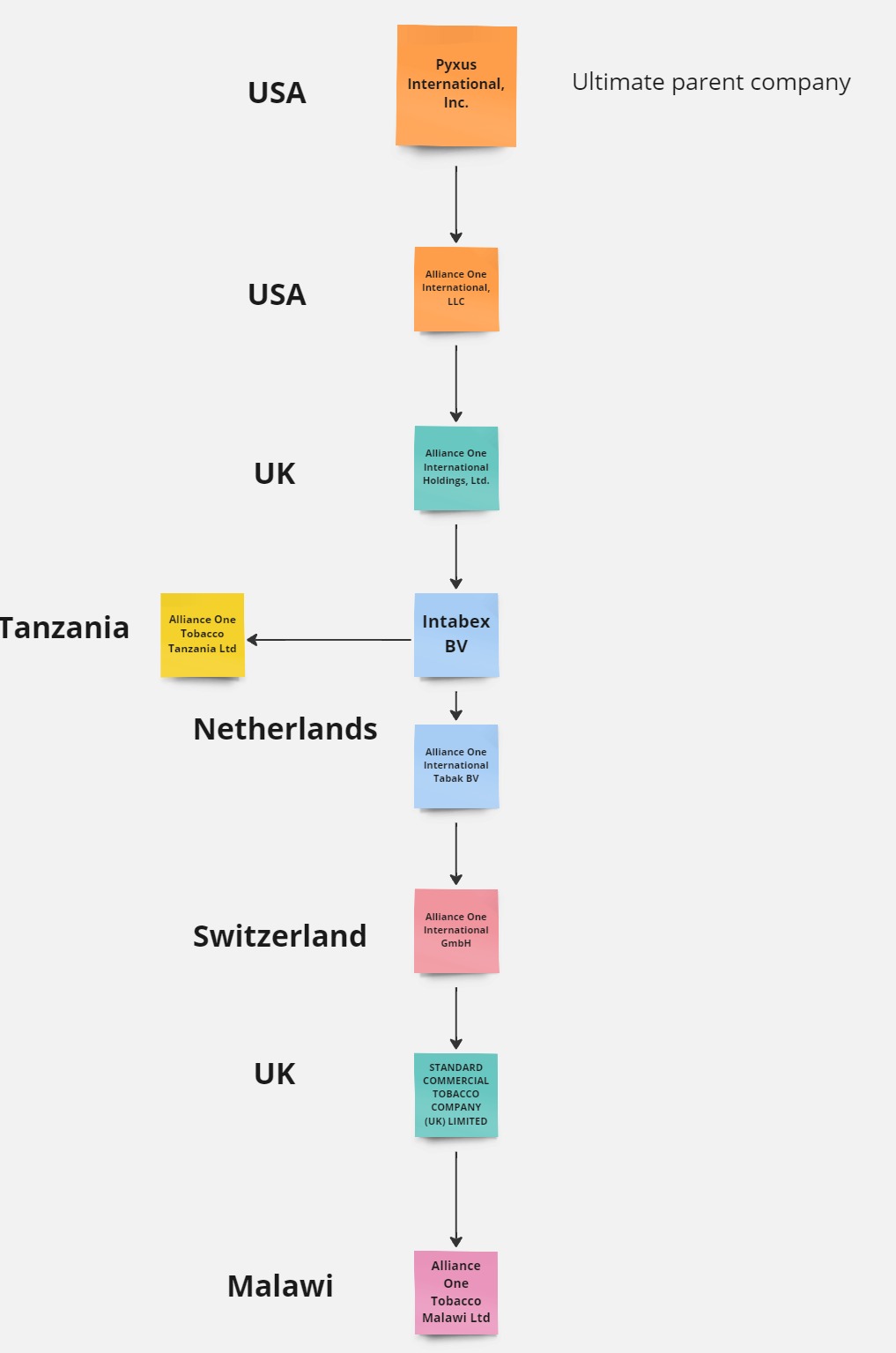

It’s uncertain where the payments went. There are three subsidiaries located in tax havens – Switzerland and the Netherlands – between AOTM and its ultimate parent, Pyxus International.

Cost of Sales Vs. Working Conditions

The need for taxable profits for AOTM seems implausible for another reason: the business model of tobacco farming in Malawi. Since 2012, AOTM has bought leaves from farmers via contract farming, officially called the Integrated Production System (IPS). The licensed tobacco farmers get inputs, such as fertiliser, to produce tobacco leaf. The companies guarantee to buy their tobacco.

The contract conditions are pre-defined by the company. Despite having no say in the voluntary agreement, the farmers indicate they agree, hoping to fetch better selling prices.

Yet, five years into contract farming, Msukwa, a tobacco farmer who also chairs the Kamatau growing scheme, gathering over 30 clubs for AOTM on contract farming, claims the farmers have no tangible benefits to show.

“We want to improve our livelihoods and provide for our families… But AOTM is greatly benefiting from tobacco farming, more than us, the farmers,” Msukwa said.

For instance, in the 2022/2023 farming year, Msukwa received farm inputs worth about MK5 Million ($2,980) on servicing his loan, payable after tobacco sales. After sales, he repaid about K10 million ($5,950). He was left with a K2 million ($1,190) profit.

“It’s as if I only farmed to repay the loans. I got very little profit compared to the amount of money and energy I invested,” Msukwa said.

He normally expects a profit of over K6 million ($3,580). But the exorbitant contract loans, alongside unpredictable weather conditions, contributed to his losses.

Msukwa explains that AOTM loans from banks are used to buy inputs for the farmers. After selling tobacco, the company deposits the profits into the farmer’s bank accounts. The loan is immediately deducted, and the farmers get the difference. They also receive a bank statement to see the values of sales and repaid loans. When they enter contract farming, the farmers have no idea what the interest rate will be.

“When you’re in contract farming, you’re trapped. You have no say about your tobacco. It’s obviously a loss to the farmer,” he stated.

Msukwa adds that in 2023, the farmers noticed that contract farmers bought tobacco at slightly lower prices than those not on contract. The farmers tried to speak with AOTM about the unfair contract conditions, but to no avail; they either had to accept them or leave.

The company denied that its contract system is exploitative to the farmers. AOTM states, “We keep the farmer at the heart of everything we do”, adding that farmers can accept or decline the contracts offered. According to AOTM, the contracts are provided in English and two other local languages for the farmers’ understanding.

Since 2019, there has been an ongoing court case in which Malawian farmers, represented by United Kingdom-based law firm Leigh Day, accuse British American Tobacco (BAT) and Imperial Tobacco of facilitating “unlawful and dangerous [working] conditions’. The farmers claim to work from 6 am to midnight every day of the week, live on too little food, be forced to build their own homes, and still get paid nothing at the end of the growing season. The lawyers running the case, Martyn Day and Oliver Holland, explained that about 70% of the farmers they represent worked on AOTM farms because the company supplies both BAT and Imperial Tobacco. Our trade data analysis confirms this. Per Martyn Day, the labour abuses “are endemic to Malawi due to the way the tobacco system is set up.”

“[Leaf-buying companies] do what they can to get low-cost leaf at the lowest labour price possible,” Otañez states. It’s hard to see what operational costs would reduce the profits to the extent that AOTM paid no taxes. Predominantly as the company exports raw tobacco, which means few costs for processing.

Precedent in Tanzania

A court case from a sister company of AOTM, Alliance One Tobacco Tanzania Ltd (AOTT), is illustrative. Tanzanian tax authorities audited AOTT’s financial statements in 2005 and 2011. The authorities questioned several of the company’s corporate tax items. Most importantly, the auditors said there wasn’t enough evidence of the costs the company incurred for its sales. Those costs made AOTT entitled to tax relief.

AOTT objected to the ruling, stating that “the disallowed costs were deductible as they were wholly and exclusively incurred in the production of the income”. However, the company failed to provide evidence for the costs, such as invoices. Their objection was, therefore, rejected, the appeal case dismissed, and AOTT was ordered to pay the appeal’s costs.

Both tax experts Kiezebrink and Michel state it’s “very feasible” that AOTM is behaving similarly to its Tanzanian sister company.

“I think that’s a pattern replicated everywhere in the African countries that produce for these [multinational] companies,” Otañez states. “It doesn’t surprise me. The only surprise is that this kind of knowledge leaks in these [court case] details.”

Impact on Malawi

Social accountability expert Chigwenembe says AOTM’s tax non-compliance is reducing Malawi’s already vulnerable capacity to develop. “Tax non-compliance cripples our government’s potential to invest in sectors that are important to Malawi citizens. The government fails to invest in the health, agriculture, and education sectors due to limited resources.”

The lost tax money is vital for the Malawi government to improve essential services, such as fixing the collapsing health system, sustaining quality education, and investing in the agriculture sector. A functioning public sector is even more crucial to supporting farmers in abusive farming schemes.

However, “tax authorities also play a role in combating tax avoidance and evasion,” Jan van Koningsveld, founder of the Offshore Knowledge Center, stated. “For example, by conducting more and better audits.”

In the leaked document, we can see that AOTM has received no penalties from the MRA.

Michel explained that “[penalty] procedures are complicated and take very long. Three years after 2020 [when AOTM paid no CIT], it’s too soon to say anything about penalties.”

Chigwenembe highlights that AOTM’s tax issues expose Malawi’s weak system, which allows multinational companies to continue with malpractices. He calls on reforming the tax system. “There are several multinational companies that have been, and are still evading tax in Malawi. It’s just a matter of implementing existing policies and laws to deal with this. But the system is failing on enforcement.”

In January 2024, MRA suspended its six officers over tax fraud. They forged tax exemption certificates, to claim taxpayers’ money refunds.

Right to Reply

AOTM denied any wrongdoing, emphasising that they paid all due taxes to MRA in 2020 and 2021. According to Corporate Affairs Manager Francoise Malila, AOTM supports the growers, including the provision of inputs, certified seed, approved fertilisers, personal protective Equipment, and crop protection agents, which are sourced in bulk at a discount favourable to the farmers and delivered to their farms.

AOTM confirmed that loans for IPS come from Malawian commercial banks. AOTM acts as a guarantor.

“Within AOTM’s IPS program, growers can select between two financing levels – full and reduced package options. We stress that we don’t force growers to contract with AOTM; access to the loan package is voluntary,” Malira said. The input costs, including the loan value, are clearly defined in the contract, she added. There is also an indication of minimum grade prices based on the prior season.

“It is important to note that the Tobacco Commission regulates the Integrated Production System (IPS) in Malawi. The regulator approves all IPS contracts before contracts are offered to growers affiliated with tobacco grower associations”, the company underlines. However, the organisation itself acknowledges some challenges in this process.

“We are currently looking into various issues related to contracts that tobacco farmers and buying companies enter. These are internal discussions aimed at providing clarity on several aspects and at ensuring that, overall, contracts benefit the industry in Malawi,” said TC Public Relations Officer Telephorus Chigwenembe.

Msukwa, however, stated: “We, of course, benefit somehow because we couldn’t afford the inputs. If we had sustainable means to grow tobacco without the companies, we wouldn’t involve them.”

Msukwa and others are considering quitting contract farming as it’s no longer profitable. Yet, farmers can’t get out. Despite barely making a profit, farmers, including Msukwa, believe no crop is more profitable than tobacco in Malawi.

If AOTM also claims not to turn a profit, it means that money earned off Malawian farmers’ backs ends up stacked in the Global North instead of invested back into Malawi.

This collaborative cross-border investigation was supported by CiFAR: Civil Forum for Asset Recovery in the framework of the Investigate East and Southern Africa programme.

.png)